Orange County 2Q 2024 Industrial Market Report

OVERVIEW

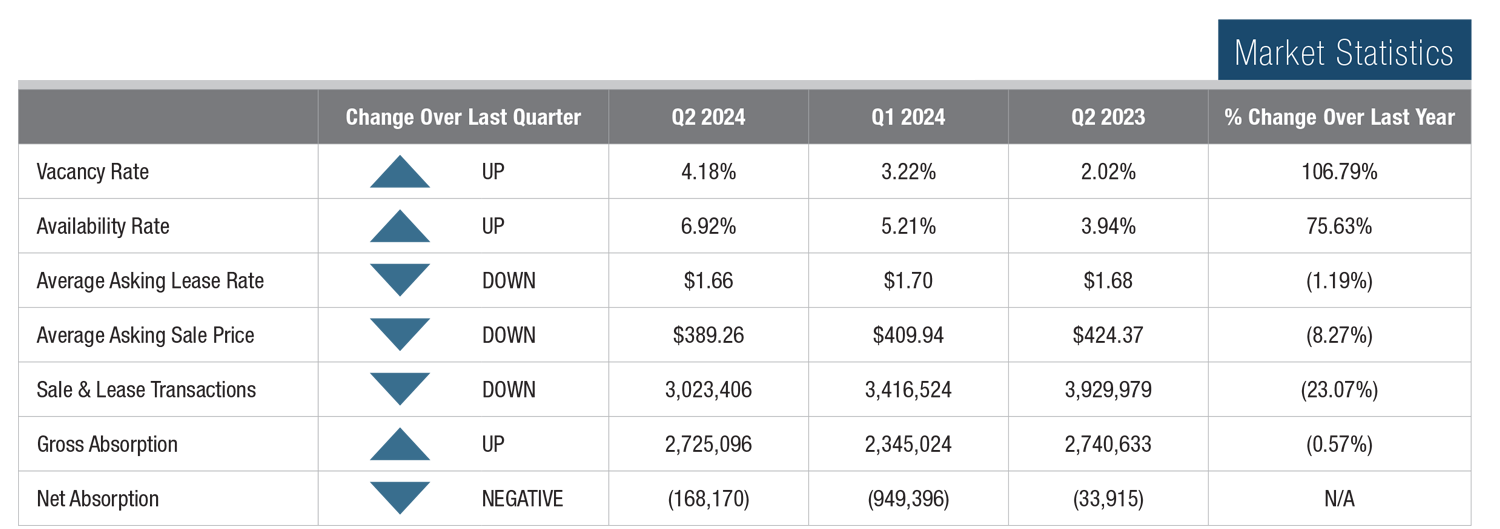

The Orange County industrial market softened further in Q2. Net absorption remained negative and vacancy rose again. The number of sales remained steady, but lease transaction count declined. Brokers report another drop in active lease and sale requirements, which is putting additional downward pressure on lease rates and sales prices. More deliveries in the Airport Area contributed to the spike in vacancy and an increase in the availability of premium space at the highest asking rates. Time on market increased again, prompting landlords to increase tenant and broker incentives. SBA mortgage interest rates for owner/user properties softened a bit late in the period, but not enough to cause a measurable interest in activity. The SBA 504 mortgage rate dropped to 6.35% in June from 6.69% in April.

VACANCY & AVAILABILITY

Orange County’s industrial vacancy rate jumped by 96 basis points to 4.18% in Q2 after a 65-basis-point rise in the first quarter. Year over year, vacancy has more than doubled but remains low by historic standards. That said it is the pace of the increase that is cause for concern, especially if this trend continues. The supply of high quality buildings offered for sale remains thin, but time on market is on the rise across the board, which contributes to rising vacancy and availability. The availability rate rose 171 basis points over the quarter, to 6.92%. This is primarily due to the increase in time on market and the delivery of several new buildings in the Airport Area during Q2.

LEASE RATES & SALES PRICES

The average asking lease rate countywide fell by another $0.04 in Q2 after a $0.09 drop in Q1, ending the current period at $1.66. For the first time in more than a decade, year-over-year average asking lease rates declined. Though the decrease was only 1.2%, it reflects the shift in underlying market dynamics. Landlords are reducing rates while they also increase tenant concessions to get their buildings leased before rates fall further. The average asking sales price also declined in Q2, falling to $389 per square foot from just under $410 per square foot in the first period. Year over year, the average price of an industrial building countywide fell by 8.27% after consecutive year-over-year gains since 2011. Sellers face pressure to reduce prices as high mortgage rates persist and inventory grows. Price cuts during marketing are becoming common, and even competitively priced properties struggle to attract buyers. The market is challenged by buyer hesitation due to high rates and fears of a potential economic downturn affecting property values.

TRANSACTION ACTIVITY

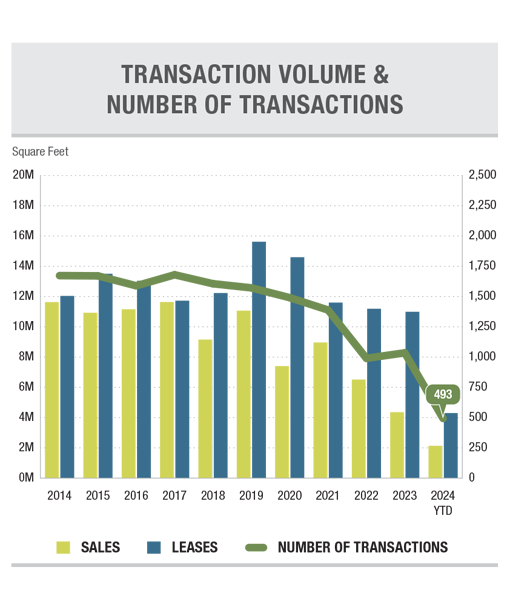

Sale transaction velocity was flat in Q2 with 38 buildings changing hands in the period. Owner/user activity remained sluggish due to persistently high mortgage rates and a price point that does not reflect the increase in debt service. At today’s rates, an owner/user in a standard SBA scenario has a mortgage payment of $2.50 per square foot per month, excluding the higher property taxes associated with the sale. Depending on the building, that can be as much as double what the rent would be for the same building. Unless prices come down substantially, that gap will remain large enough to discourage building ownership. Overall lease and sale activity by square footage fell by almost 400,000 SF in Q2, ending the quarter at 3,023,406 SF, the lowest quarterly total in several years.