Mid-Counties 4Q 2020 Industrial Market Report

Overview

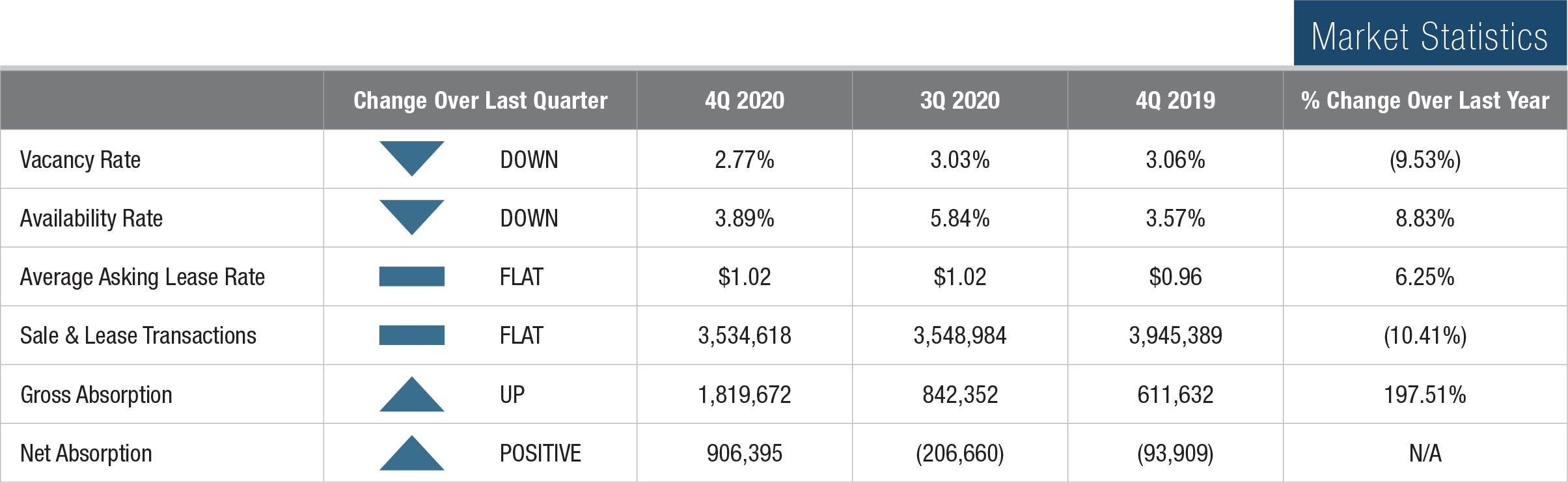

Activity in the Mid-Counties industrial market maintained its strong pace in the final quarter of 2020. Lease and sale transaction activity mirrored a strong performance in Q3. Lease rates were unchanged and vacancy made a modest decline. Gross absorption was way up and net absorption returned to positive territory. Despite another pandemic shutdown in Los Angeles County, industrial business owners kept their foot on the gas to meet surprisingly strong demand for goods and services. The Mid-Counties market has been tightening for the last few years, sending supply to record lows, while construction of new inventory has not kept pace with demand for quality space. Owner/user purchase activity accelerated in Q4, as buyers were anxious as ever to lock in fixed-rate mortgages at historically low interest rates.

Activity in the Mid-Counties industrial market maintained its strong pace in the final quarter of 2020. Lease and sale transaction activity mirrored a strong performance in Q3. Lease rates were unchanged and vacancy made a modest decline. Gross absorption was way up and net absorption returned to positive territory. Despite another pandemic shutdown in Los Angeles County, industrial business owners kept their foot on the gas to meet surprisingly strong demand for goods and services. The Mid-Counties market has been tightening for the last few years, sending supply to record lows, while construction of new inventory has not kept pace with demand for quality space. Owner/user purchase activity accelerated in Q4, as buyers were anxious as ever to lock in fixed-rate mortgages at historically low interest rates.

Vacancy/Availability

If there is anything holding the Mid-Counties market back, it’s low vacancy. The entire market is starved for space. The overall vacancy rate fell 21 basis points in Q4 to just 2.77% after a slight increase in the previous period. The pandemic crisis has had little effect on market performance. Santa Fe Springs, the region’s largest submarket at 53 MSF, saw its vacancy rate plummet to just 1.89%, which is forcing tenants and buyers to expand their search areas to include Orange County and the Inland Empire. Tight conditions continue to keep the brakes on net and gross absorption, forcing those tenants who need to stay in the area to renew in place or hold their owned properties, even if it impacts efficiency and productivity. The availability rate (vacant space plus occupied space offered for lease or sale) also moved sharply lower, in part because several larger available buildings leased or sold before becoming vacant.

Lease Rates

The average asking lease rate in the Mid-Counties was unchanged in Q4, at $1.02. Landlords are still taking a hard line on lease negotiations, but some are willing to offer minor concessions on free rent and tenant improvements. Tenants continue to pursue turnkey deals that minimize downtime. So, those landlords willing to spend upfront money on refurbishing older buildings are getting their spaces leased up quickly. Spaces from 25,000 to 50,000 SF saw a rate rise of $0.05 to $1.12, while the larger size categories ranged from $0.87 to $0.93, a slight decline since the end Q3. Absolutely no space is available between 250,000 to 500,000 SF, and there is just one offering over 500,000 SF. The true average lease rate is probably higher due to the fact that many properties, some of them of the highest quality, are offered without an asking price to encourage competition between multiple tenants.

Transaction Activity

The number of lease transactions completed in Q4 was relatively flat at 106, but sales transactions moved up to 22 from 18 in Q3. Only the lack of available buildings for sale is keeping that total from moving much higher. Total square footage leased rose to 2.9 MSF from 2.1 MSF in Q3. That is due to larger transactions being done as bigger tenants, who were uncertain about the pandemic’s business impact earlier in the year, are now more confident in their ability to generate revenue going forward.