Orange County 3Q 2021 Industrial Market Report

Overview

The Orange County industrial sector remained on course in 3Q. Demand remained intense, supply shrank, vacancy fell, and prices moved sharply higher. In other words, things haven’t changed much. OC business owners are still in expansion mode, if only they could find quality space for their operations. Even another surge in the virus didn’t slow things down. In fact, active requirements for lease and owner / user purchase opportunities moved steadily higher as the quarter progressed. That sent lease rates and sales prices to new record highs. While e-commerce drove activity early in the pandemic crisis, users across the entire industrial spectrum are now experiencing healthy growth. The biggest problem for Orange County business owners is the lack of supply of quality industrial space. The existing base of inventory is stretching to meet demand and construction activity remains light.

The Orange County industrial sector remained on course in 3Q. Demand remained intense, supply shrank, vacancy fell, and prices moved sharply higher. In other words, things haven’t changed much. OC business owners are still in expansion mode, if only they could find quality space for their operations. Even another surge in the virus didn’t slow things down. In fact, active requirements for lease and owner / user purchase opportunities moved steadily higher as the quarter progressed. That sent lease rates and sales prices to new record highs. While e-commerce drove activity early in the pandemic crisis, users across the entire industrial spectrum are now experiencing healthy growth. The biggest problem for Orange County business owners is the lack of supply of quality industrial space. The existing base of inventory is stretching to meet demand and construction activity remains light.

Vacancy/Availability

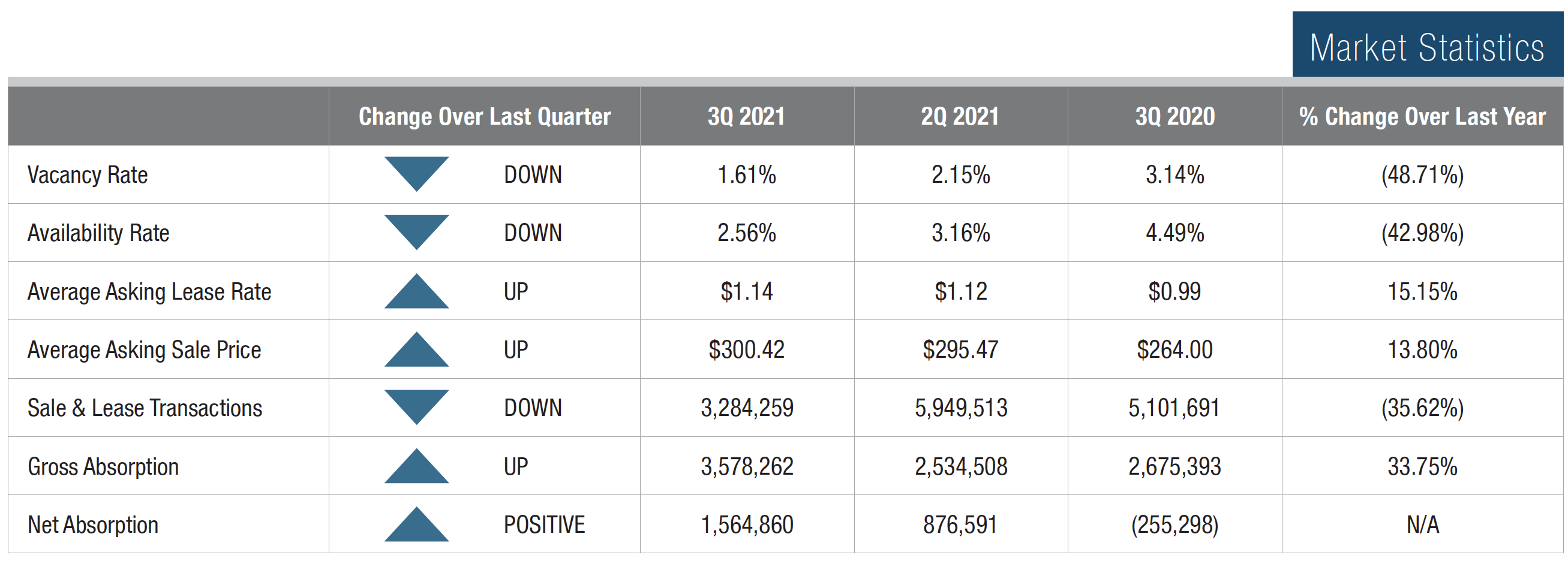

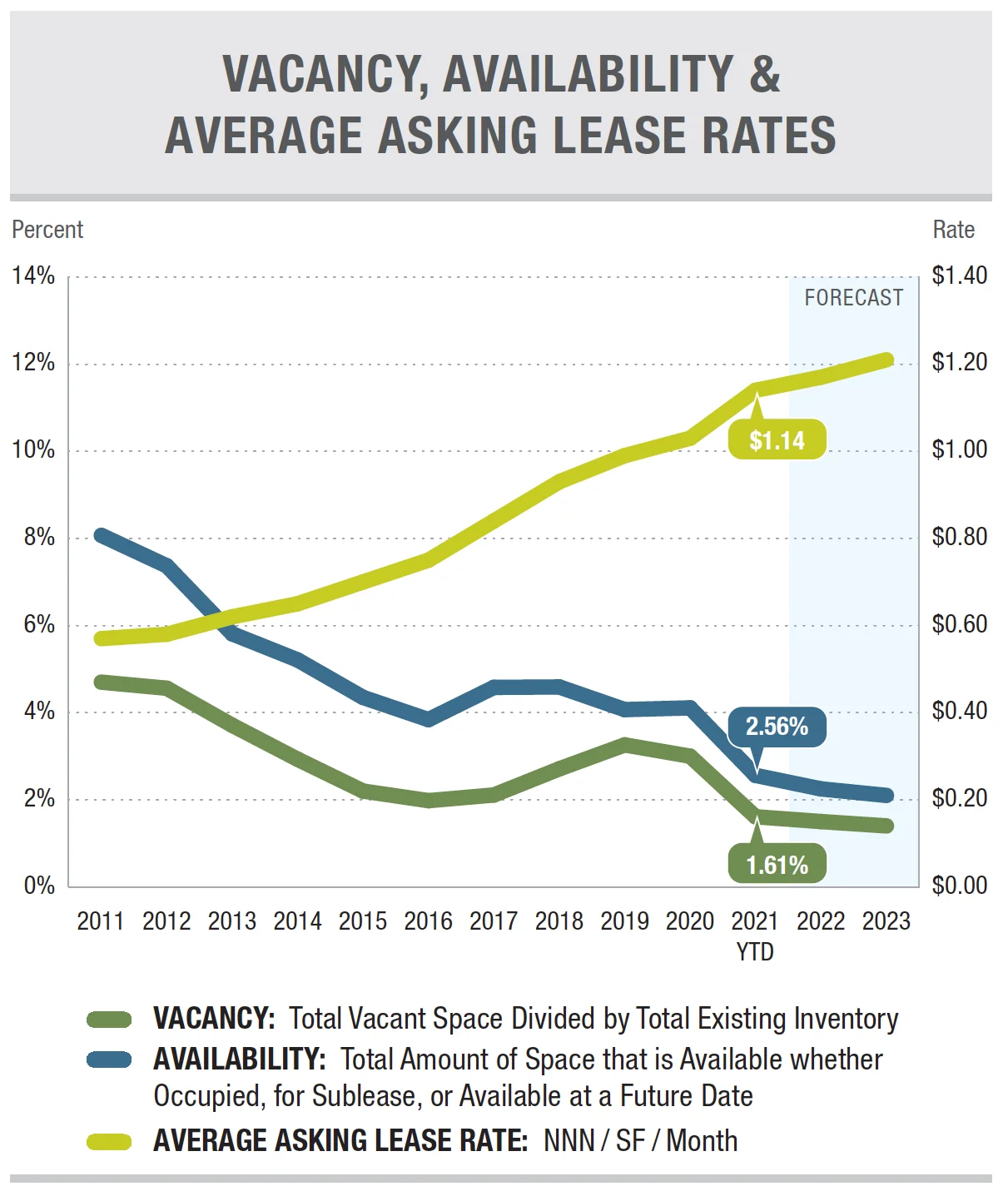

The overall vacancy rate in Orange County fell to 1.61%, a 54-basis-point drop from the previous quarter. Some of the available space is functionally deficient in one way or another, so from a practical point of view, the vacancy rate is approaching zero in many Orange County cities. Tenants and buyers continue to compete aggressively for product. It is not uncommon for landlords to consider ten or more offers on their properties. The availability rate, which includes space offered for lease or sale but is still occupied, fell to 2.56% from 3.16% in 3Q. That tight spread to the vacancy rate indicates an increase in lease renewals and fewer properties being offered for sublease.

Lease Rates & Availability

The average asking lease rate for the county added another $0.02 to $1.14 in 3Q, breaking yet another record. Landlords still have the upper hand in lease negotiations, and they are holding the line on concessions, with many deals being struck without free rent or tenant improvement contributions. With such intense competition for space, it is common for final lease rates to be well above asking. It is also important to note that many buildings are offered for lease without an asking rate, and those tend to be of higher quality. As a result, actual rents are somewhat higher than reported.

The county’s average asking sales price broke the $300 per square foot barrier for the first time in 3Q, moving up to $300.42 from $295.47 in 2Q. However, many properties are sold on an off-market basis and they are selling for well above $300 per square foot depending on size and location. Suffice it to say, the sale market is on fire and buyers continue to bid aggressively.

The county’s average asking sales price broke the $300 per square foot barrier for the first time in 3Q, moving up to $300.42 from $295.47 in 2Q. However, many properties are sold on an off-market basis and they are selling for well above $300 per square foot depending on size and location. Suffice it to say, the sale market is on fire and buyers continue to bid aggressively.

Transaction Activity

Lease and sale activity both in terms of square footage and number of transactions fell sharply in 3Q after a strong second quarter. However, that is due in large part to the lack of supply, which has hamstrung industrial users from signing new leases and purchase contracts. Just 3.3 MSF of deals were inked during the current period, down from over 5.9 MSF in 2Q. In all, 258 transactions were completed during the period; 183 leases and 75 sales, as compared to a total of 277 leases and just 101 sales in 2Q. The largest deal of the period was a 395,000 SF sale to CBRE Global Investors at 17871 Von Karman Avenue in Irvine. Another 106,000 SF building in Anaheim was sold as an investment to Penwood Real Estate Investments Management by Camphor Partners.